When central banks increase interest rates in response to high inflation, it almost always causes a recession. Since central banks in Europe, Canada and the United States increased interest rates sharply over the last half of 2022, many economists expected 2023 to open in a recession for these economies.

When central banks increase interest rates in response to high inflation, it almost always causes a recession. Since central banks in Europe, Canada and the United States increased interest rates sharply over the last half of 2022, many economists expected 2023 to open in a recession for these economies.

Despite these predictions, global economic growth has been more resilient than forecasters expected, and unemployment is historically low in the European Union and North America. But while we may not be in a recession yet, we’re starting to see signs that economic growth is slowing.

Forecasters at major Canadian banks are now predicting that Canada’s economy will experience two quarters of near zero or negative real economic growth in 2023.

Provincial forecasts predict that British Columbia, Ontario and Quebec will be hit the hardest. Since both Ontario and Quebec rely heavily on their trading relationships with the United States, a slowdown in the US will translate into less economic activity in these regions. Meanwhile, Ontario and BC have the highest cost of home ownership in the country. High interest rates have slowed the real estate market in these provinces and are putting pressure on household budgets.

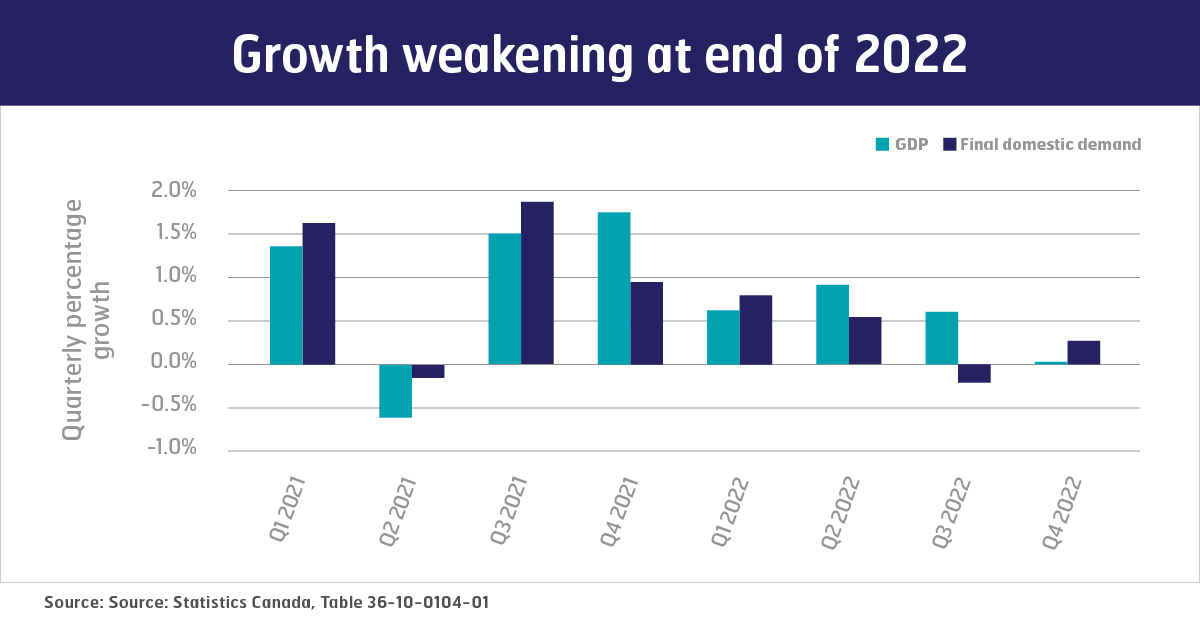

Data also shows that our economy is not in a strong position. Change in the gross domestic product, or GDP, is often used to approximate how healthy an economy is. GDP is the total value of the goods and services produced in a country during a specific time. Adjusted for inflation, GDP growth in Canada slowed to almost zero in the fourth quarter of 2022.

Looking into the details behind overall GDP growth shows signs of future weaknesses. Final domestic demand is the total amount of money that is spent on goods and services by the people, companies and government in a particular country. It measures the strength of domestic purchasing by excluding build-ups of inventories and exports of goods and services. Comparing final domestic demand to GDP can show us if there are economic weaknesses coming from changes in exports or inventories. While final domestic demand improved in the fourth quarter of 2022, the dynamics behind this suggest a continued slowing of economic growth. GDP was higher than final domestic demand in the third quarter of 2022 because businesses were building up inventories that they hadn’t been able to sell. In response, businesses slowed new production in the fourth quarter. Higher domestic demand in the final quarter of 2022 shows that businesses have been able to sell some of their built-up inventories, but the slowdown in production lowered overall GDP growth.

Real business investment also shrank in the third and fourth quarters of 2022, partly in response to higher interest rates. After adjusting for inflation, businesses invested less in residential structures, machinery and equipment.

So what does this mean for workers? Things are tough—but are we in a recession?

While economic growth is expected to be weaker in 2023 than it was in 2022, this slowdown may not qualify as a recession. A common definition of a recession is two consecutive quarters of negative economic growth. But that’s not a fixed rule. In Canada, the C.D. Howe Institute’s Business Cycle Council decides when a recession starts or ends. They look for a “a pronounced, persistent, and pervasive decline in aggregate economic activity” to declare a recession. This means if trends continue, including a stronger than expected American economy, Canada may avoid a 2023 recession.

However, the most recent unemployment and inflation data from the US shows that there is a significant risk that their interest rate hikes will continue, even as some US and European banks are showing the strain from higher interest rates. Continued US interest rate increases make a recession in the US more likely, which would negatively affect Canada’s economy.

Whether we are officially in a recession or not, provincial governments will be pressured by banks and economists to limit spending as long as inflation is above the Bank of Canada’s target of 1-3%. Some governments may suggest that this means they have to be cautious with upcoming budgets. It will be important to remember that the bottom line for all provinces has been significantly improved over 2022. Despite economic challenges, governments still have the room needed to invest in public services, which support our economy in the long run.