The way the Canadian tax system is structured helps the rich get richer. It also robs us of billions of dollars in revenue we need to pay for strong public services and infrastructure. The most extreme example of this is how capital gains are taxed.

Capital gains are taxed at a much lower rate than employment income, and even at a lower rate than dividends. Comparing how these forms of income are treated shows us how extreme the capital gains benefit is for the wealthy.

Capital gains and dividends are both forms of income that come from wealth rather than employment. Capital gains come from the increase in the value of property, usually real estate or stocks, at the time of sale. Dividends are a portion of a company’s profit that is passed on to shareholders. Most countries tax capital gains at rates higher than or equal to dividends, but Canada is a notable exception.

The amount of tax paid on dividends is calculated using the recipient’s marginal tax rate. However, the tax paid is reduced by a dividend tax credit. The credit is meant to account for corporate income tax that is assumed to have been paid. This means dividends are almost always taxed at a lower rate than employment income, because the dividend tax credit assumes the company paid the statutory corporate income tax rate, rather than using the actual, and lower, effective tax rate. The size of this tax loophole depends on the ability of the firm to reduce its tax owing, either through legitimate deductions, aggressive tax avoidance strategies, or in some cases, outright tax evasion.

Originally, capital gains were not subject to personal income tax at all. The 1966 report of the Royal Commission on Taxation recommended that income be taxed at the same rate no matter its source, with the chair, Kenneth Carter saying, “a buck is a buck is a buck.” By the time tax reform was implemented in 1972, many of the commission’s recommendations had been watered down, with only half of income from capital gains made taxable. The proportion of capital gains considered taxable increased to 75 per cent by 1990, but the federal Liberal government cut it back to 50 per cent in 2000.

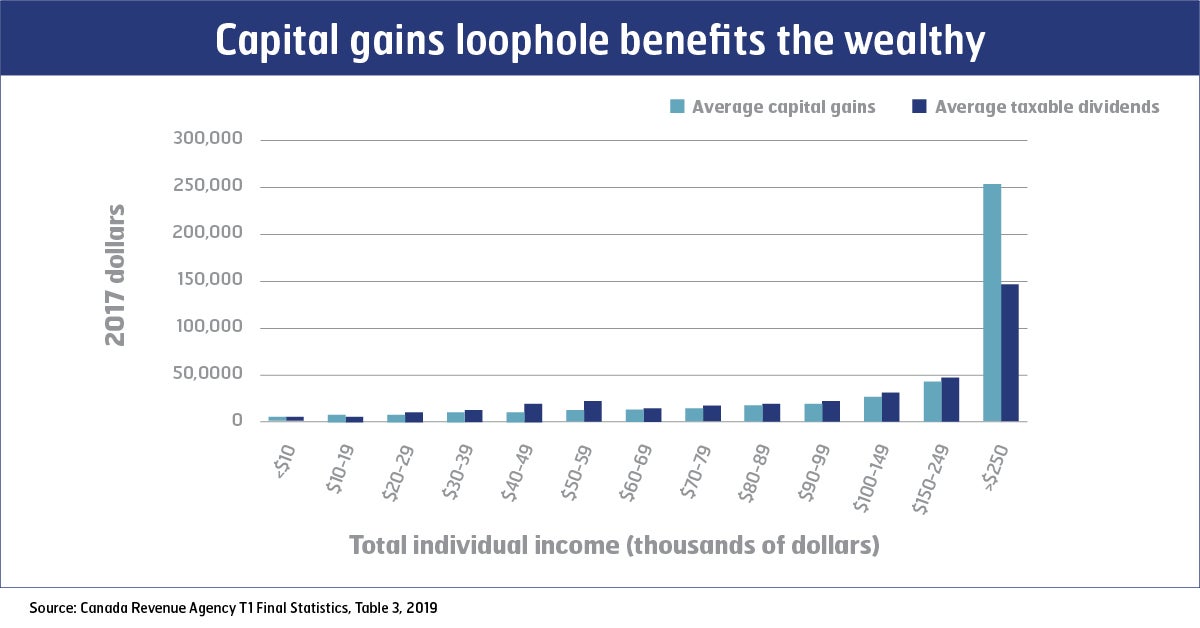

This chart shows the average capital gains and taxable dividends for individual income groups. It only includes people who had income from these sources. As this data reveals, income from capital gains is even more unequally distributed by income level than income from dividends, which might be expected given the more favourable tax treatment.

Even though they are very different forms of income, creative accountants can set up structures that turn corporate income into capital gains – called ‘surplus stripping.’ Being able to cut your tax rate in half and earn income tax-free provides a very strong incentive for rich people to establish this kind of avoidance structure. Academic research estimates that 88 per cent of the benefit of this loophole goes to the top one per cent of income earners.

There is no evidence that justifies this favourable tax treatment for capital gains. Since capital gains are based on the value of the property, there is no corporate income tax that has already been paid in the same way that there is for dividends. Those in favour of the status quo will argue that investors should be rewarded for the risk they take in making investments, but research shows that taxing a higher proportion of capital gains does not discourage investment.

By returning the capital gains inclusion rate to 75 per cent, the federal government could raise $10 billion in additional revenue every year that we could use to make smart investments in much needed public services. It would also make the tax system more fair for us all.