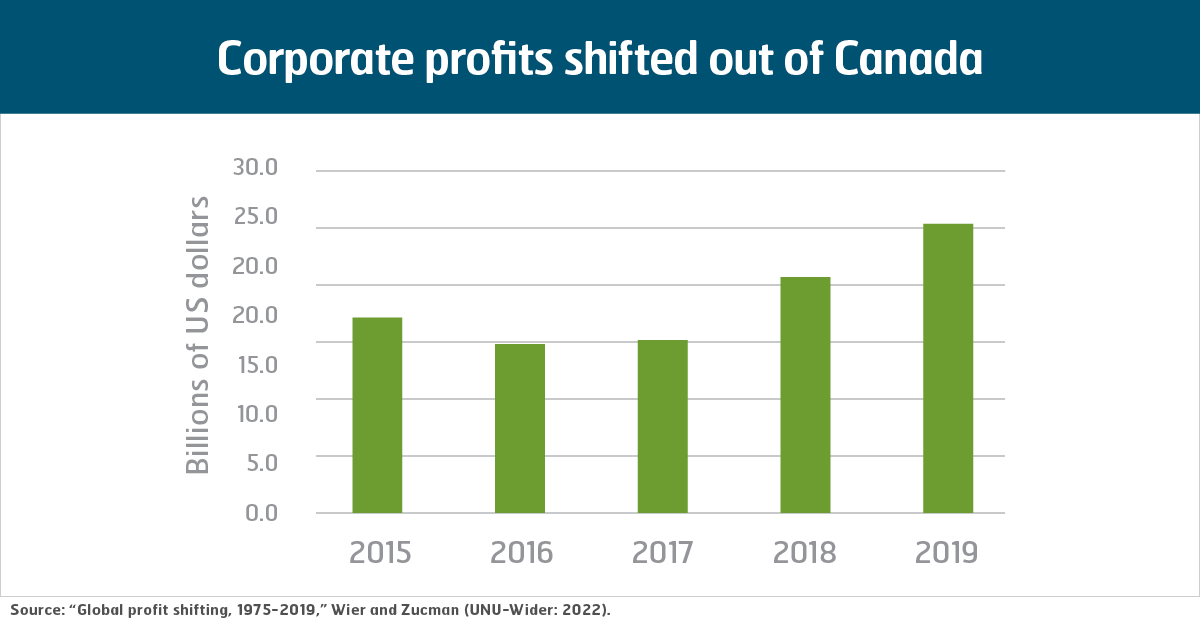

Every year, governments across the globe miss out on an estimated $240 billion USD in revenue due to companies avoiding or evading taxes. Prominent tax economist Gabriel Zucman estimated that corporations shifted more than $25 billion USD in profits out of Canada in 2019 by reporting income earned in Canada in another tax jurisdiction. This cost us an estimated $4.5 billion CAD in corporate income tax revenue for 2019 alone.

The Organization for Economic Co-operation and Development (OECD) and the G20 have been trying to fix this issue for over a decade. We’re coming up to some critical deadlines for implementing their solutions.

The OECD and G20 have established a two-part plan, with input from over 140 nations. The two parts of the plan are called Pillar 1 and Pillar 2.

Pillar 1 aims to make multi-national corporations pay appropriate taxes where their customers are located, and not just where taxes are lowest. This is crucial for Canada’s domestic businesses, which pay taxes that international giants like Amazon and Google have so far been able to avoid.

Pillar 2 seeks to eliminate the use of tax havens, partially by setting a global minimum tax rate of 15% for multinational corporations.

Pillar 1 was supposed to be in place in mid-2023. However, the United States opposes this measure and at the last meeting, in July 2023, succeeded in delaying Pillar 1. This delay includes preventing participating countries from introducing any new domestic digital taxes until the end of 2024, instead of the end of 2023. The government of Canada disagrees with this postponement. Canada promised a digital tax in 2019 and planned to launch it in 2022. The Canadian government had already pushed this deadline back to January 1, 2024, in hope of negotiating an international agreement but is unwilling to delay any further.

Fortunately, the United States is more supportive of Pillar 2. A framework for new laws and a tool for updating existing treaties to make them consistent with the agreements reached under Pillar 2 should be ready by mid-2024. Although Canada pledged in the 2023 federal budget that it would introduce Pillar 2 legislation, it has not yet done so.

Frustrated with the delays on Pillar 1, the United Nations (UN) passed a resolution in late 2022 to advance international tax cooperation themselves. The Secretary-General issued a report in July 2023 with three UN-member led options: 1) a binding multilateral convention on tax, 2) a binding framework convention on international tax cooperation, or 3) a voluntary framework for international tax cooperation. The UN plans to discuss a new resolution to implement one of these options later this year.