Inflation in January 2022 reached a high of over 5 per cent. This is putting pressure on the Bank of Canada to increase interest rates.

Most economists think inflation is caused by too much money in the economy. Central banks try to solve this problem by raising interest rates. Raising interest rates makes borrowing money more expensive and increases returns on savings. This causes consumers and businesses to delay spending and to borrow less. As a result, there is less money moving around in the economy and inflation decreases.

However, the inflation we’re seeing today is not being fueled by an excess of money. It is the result of supply chain disruptions and pandemic uncertainty. For workers, this situation will only compound the negative effects of increased interest rates.

There are several ways rising interest rates may affect CUPE members.

To begin, higher interest rates tend to lower consumer spending and business investments, leading to a reduction in hiring and an increase in unemployment.

The heightened cost of borrowing will also have a direct impact on workers’ personal finances.

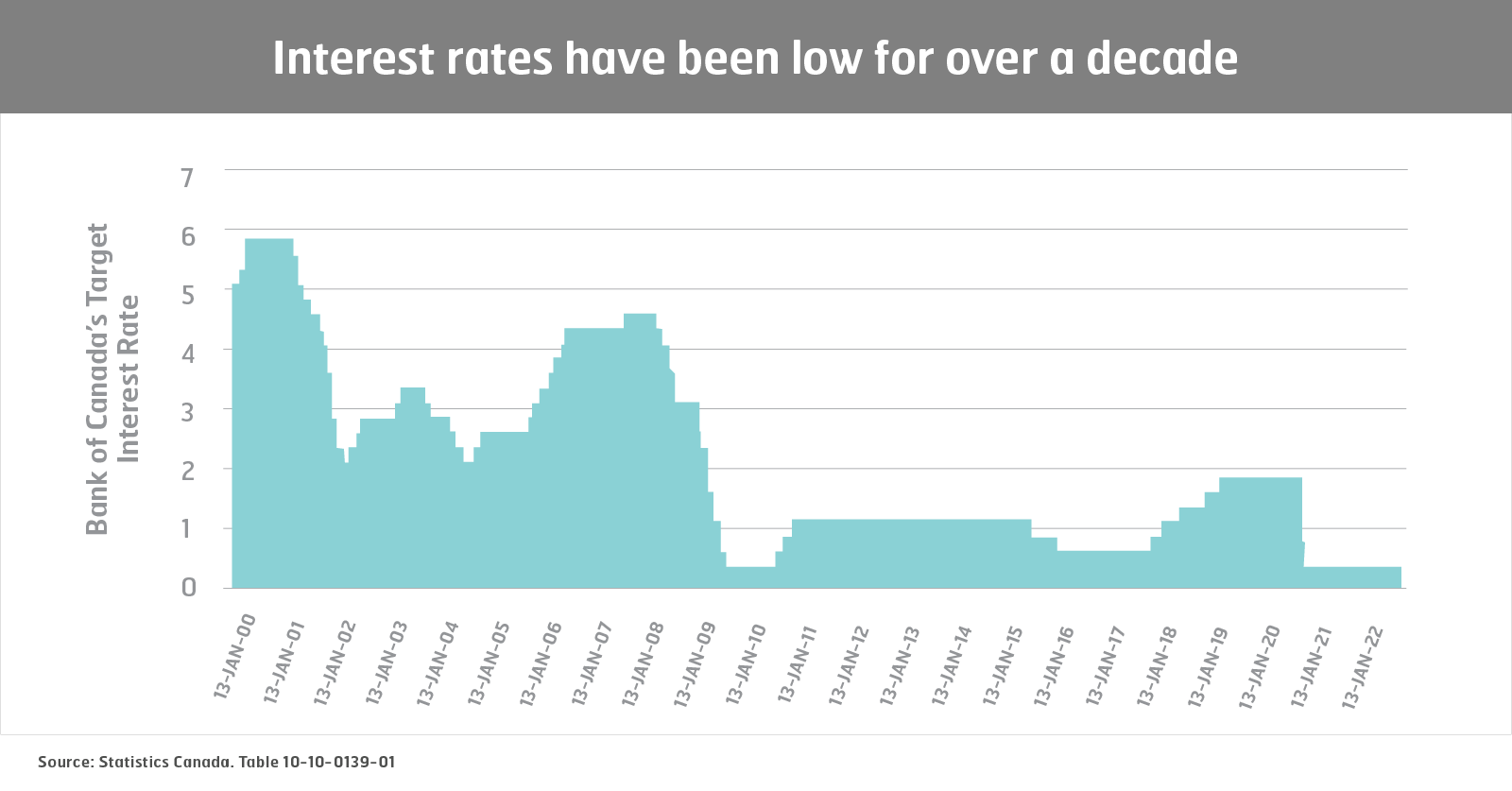

Interest rates have been low since the financial crisis in 2008, enabling families in Canada to take on significant levels of personal debt. Before 2008, the average household in Canada owed $1.49 for every dollar of income. By the end of 2021, this had risen to $1.79. Making borrowing more expensive will make it very difficult for workers to refinance this debt or to qualify for a mortgage.

We are also facing major labour market shifts due to COVID-19, automation, and responses to climate change, among other factors. While workers who have lost jobs or careers from these shifts may need to invest in education or training, rising interest rates will make student loans more costly and less accessible.

Finally, when interest rates rise, governments often become worried about spending. This happens for two reasons. First, higher interest rates make it more expensive to borrow money. Second, governments know that the central bank might think increased government spending could cause the economy to grow too fast – prompting the bank to increase interest rates even more to reverse the effect.

Even though government revenues tend to rise along with inflation, this will not necessarily translate into increased spending on public services or higher wages for public sector workers. In fact, several provincial governments are continuing to bargain with restrictive mandates and warn of cuts to public services, even after COVID-19 has illustrated the dangers of austerity and underfunding.

If the Bank of Canada increases rates to quiet fears of runaway inflation instead of as a response to data showing an excess of money in the economy, all these impacts will be intensified. Moderate increases in interest rates through 2017 and 2018 were fairly well-tolerated by workers because of a healthier economic context. The same is not true for 2022.