Housing prices, already high across Canada, skyrocketed during the pandemic. Prices rose by more than 30% between the end of 2019 and the end of 2021.

Many are hoping that rising interest rates will help cool Canada’s overheated housing market. However, this will not make home ownership more affordable for the average working family.

The amount of money that banks can lend for a mortgage is regulated by the federal government. It depends on your income and existing debt load, as well as expected heating costs and property taxes for the house you are purchasing. By law, your mortgage payments plus these other items cannot total more than 44% of your before-tax income.

Higher interest rates increase the cost of your mortgage payments, and so reduce the amount of money that a bank can offer you in a mortgage. This can add up quickly.

For a household earning the median income of $110,000, a 2% increase in interest rates would reduce their maximum mortgage by $90,000. (Median household income means that half of households make more money, and half of households make less).

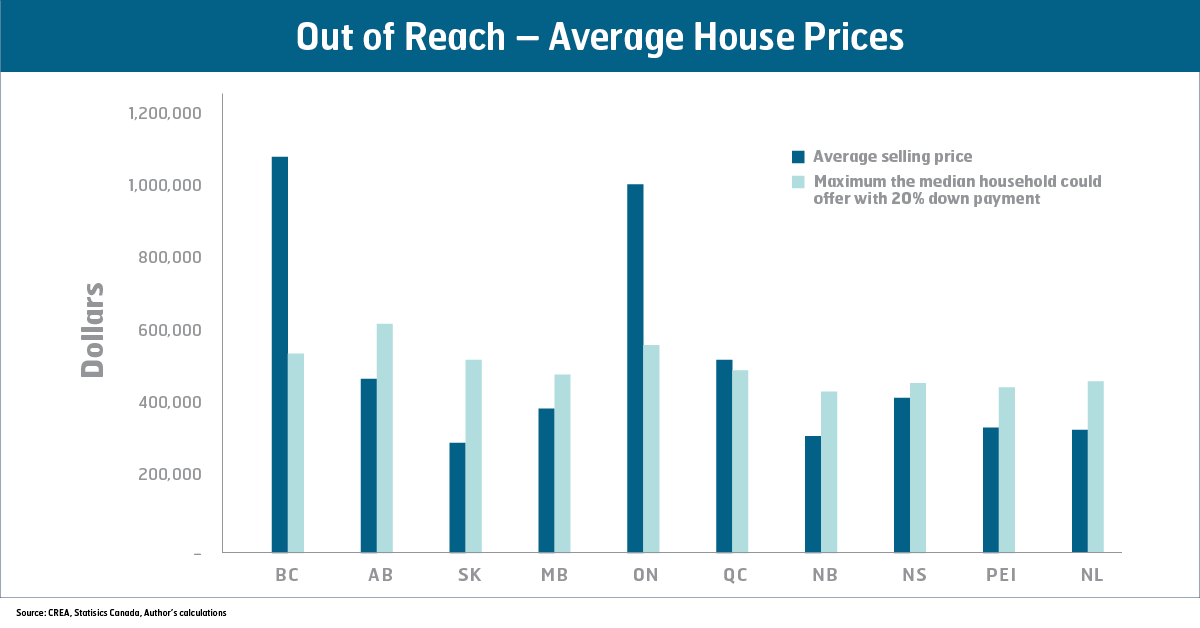

This chart shows the average price of homes sold in each province in April 2022. Next to that is the maximum offer that a household with the median income could place on a house at current mortgage rates (4.6%), assuming they had saved up a 20% down payment.

In Canada’s three largest provinces – British Columbia, Ontario, and Quebec – the average house price is out of reach for a household with the median income and a 20% down payment. Nova Scotia is getting very close to that line.

With rising interest rates, the majority of households will find themselves locked out of the housing market because there simply are no houses available at the amount they are allowed to borrow. Meanwhile, saving for a down payment will become even more difficult as rental costs surge above the affordability bar set for home ownership.