Since the mid-1990s, policy at all levels of government across Canada has been shaped by the guiding principle of reducing government debt. This is why, especially around election time, you’ll often hear politicians talk about “balancing the budget” or “fiscal responsibility.” The 2025 federal election was no exception. The opposition Conservative party accused the governing Liberals of spending too much and increasing the federal deficit to an irresponsible degree. Even some Liberals, including then-Deputy Prime Minister Chrystia Freeland, accused then-Prime Minister Justin Trudeau of overspending. After Trudeau resigned, Mark Carney campaigned on the promise of reducing or “capping” government spending in an attempt to distinguish himself from his predecessor.

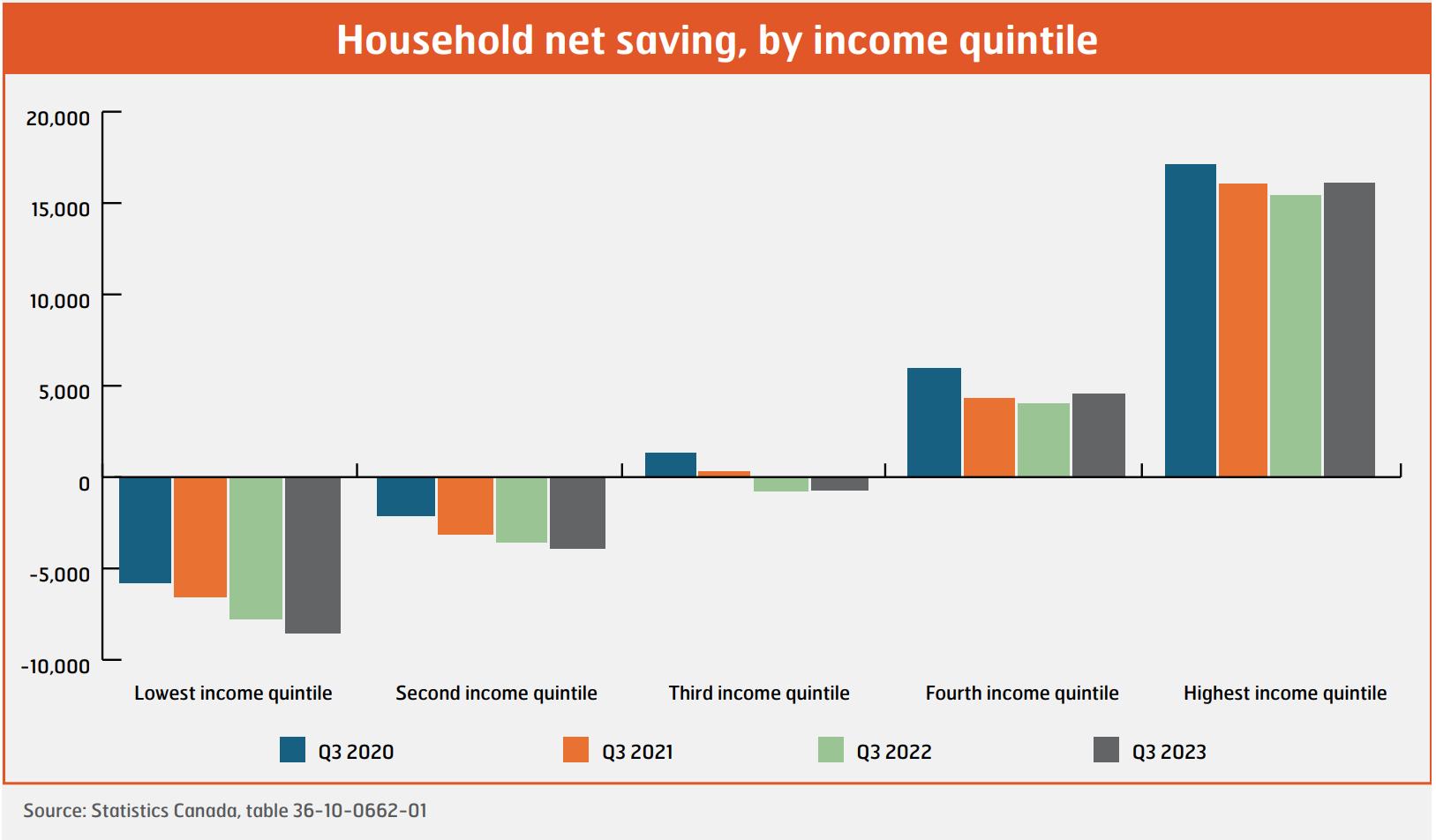

When politicians and the media stoke fear around government debt, it hits home because most of us have our own firsthand experience with debt. Common sense tells us that going into large amounts of debt, with no clear plan to pay it off, is a bad idea. Still, the total amount of debt held by Canadians has been on the rise over the past few decades. Debt is a major source of stress in many people’s lives, but unfortunately, a growing number of people rely on debt to make ends meet. While Canada’s highest earners have increased their household savings significantly over the past few years, the lowest earners have gone deeper and deeper in debt and are unable to save for their futures. However, this is not the kind of debt that governments and politicians are worried about.

The Fall 2024 edition of Economy at Work debunked some common misconceptions about government debt and its relationship to economic and societal well-being. Here are two key points we want to highlight:

- Government borrowing often supports economic growth.

- Canada has one of the lowest debt-to-GDP ratios in the G7, a sign that economic growth is being supported by government spending.

One of the ways that economists measure the impact of government spending on the economy is to compare the gross domestic product (the GDP, or the total value of all goods and services produced by a country), with the country’s net debt, which is the government’s total debt, minus the value of all government assets, like land, buildings and money. This is called the net debt-to-GDP ratio.

There is no consensus on what the ideal debt-to-GDP ratio is, no ‘magic number’ to strive for. However, generally speaking, if the economy grows faster than the government’s debt, then borrowing (debt) is likely supporting economic growth.

Another important debt measurement is the household debt-to-GDP ratio. This measures how much personal debt Canadian households have relative to the size of our economy. Out of the ten largest economies in the world, Canada has the highest household debt-to-GDP ratio – over 100%. The ratio has remained at or above 100% for over a decade. Around three-quarters of this debt comes from mortgages, but the rest includes things like credit card debt, car loans and other forms of personal or small business debt. In Canada, our personal monthly debt is growing faster than our take-home pay. No wonder we are seeing a growing gap in wealth and household savings between lower and higher earners.

Here is an important point: government and household debt are not the same thing. For ordinary people, debt is a stressful burden. But for governments, deficits are simply a normal part of operations, despite politicians’ claims to the contrary.

But these two kinds of debt are linked because efforts to reduce public debt can lead to increased household debt. For over 30 years, rather than simply reducing public debt, governments have offloaded more and more expenses onto individuals. This is because the federal and provincial governments in Canada have tried to reduce public debt primarily by cutting services, while lowering corporate taxes and eliminating other government revenue streams that make corporations and the wealthy pay their fair share.

When governments make cuts to services, the need for those services does not just disappear. Instead the cost of the programs are passed down, often to those who are in the lowest income brackets and need social programs the most. It is not a coincidence that income inequality is reaching record highs, and that low-income households are increasingly in debt. This is what happens when governments pursue debt-reduction by any means necessary. It is clearer every day that this strategy must change. Instead, government should invest public dollars to create a more equal society where people can live in dignity and comfort.