High interest rates are making it harder to afford a home. In July 2023, the Bank of Canada increased its interest rate to 5%. This is the highest it’s been since 2001.

The bank is raising rates to fight inflation. The idea is that since higher interest rates make loans more expensive, people will spend less and businesses will make fewer investments, creating fewer jobs. Less spending in turn is supposed to help slow down rising prices.

However, despite the bank’s intentions, rising mortgage rates have become one of the biggest factors keeping inflation high. Mortgage interest costs, which are included in the Consumer Price Index (CPI) basket, rose by over 30% in July compared to the previous year. According to Statistics Canada, mortgage interest costs were the single largest contributor to inflation in July. Excluding these costs, inflation would have been 2.4% instead of 3.3%.

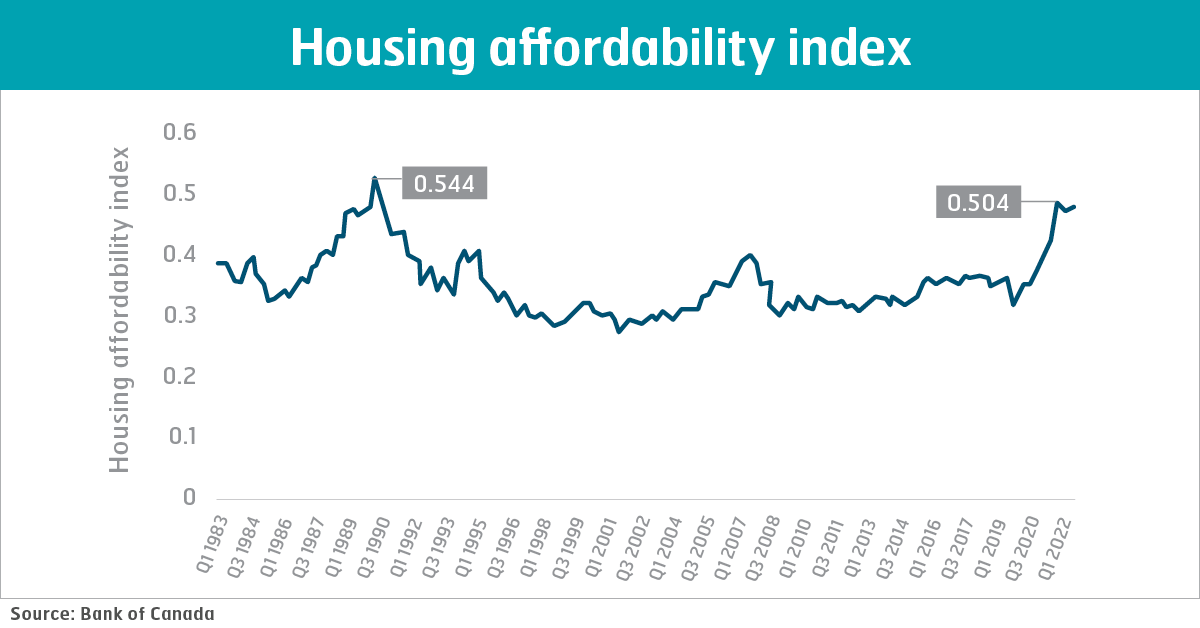

We can see how the recent increase in mortgage rates is affecting home ownership affordability by looking at the Bank of Canada’s “housing affordability index.” This index compares average mortgage payments and utility bills to the average household disposable income. To approximate average mortgage payments, the bank uses real estate data on the average resale price for all housing sold in Canada, and a weighted average of discounted fixed and variable rate mortgages.

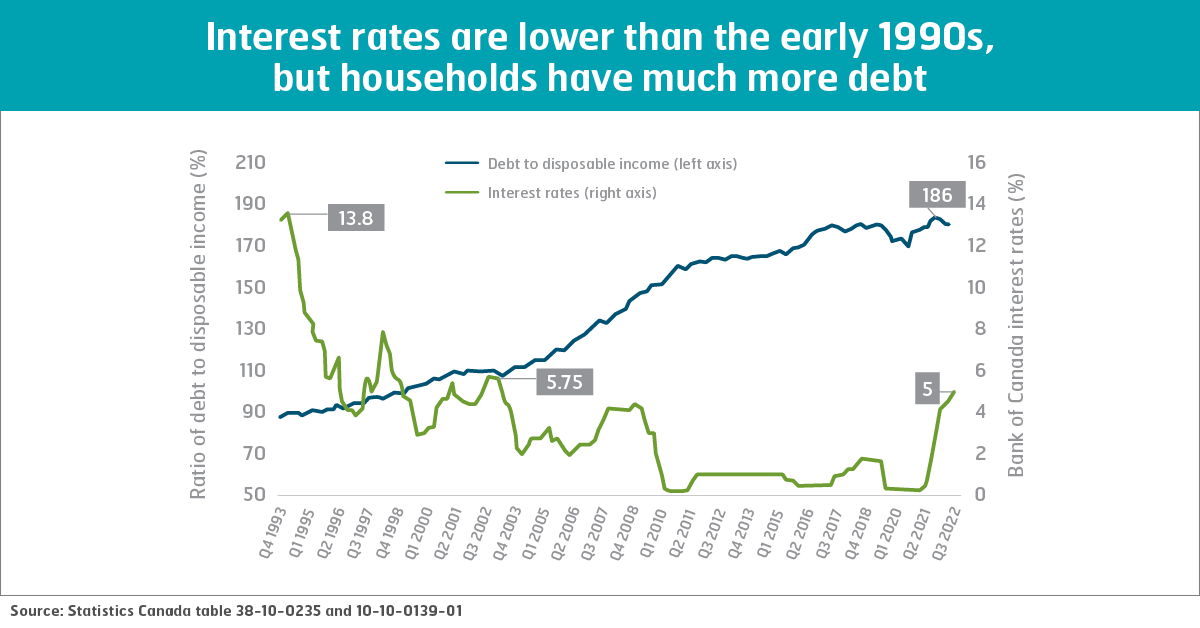

In fall 2022, this index hit just over 0.5. This means that more than half of a household’s disposable income goes to home costs. The last time it was this high was when it peaked at 0.54 in 1990. Back then, the Bank of Canada’s interest rate was over 13%.

You might ask, why are 5% rates having the same effect as higher rates in the late 1980s and early 1990s? The reason is households today have more debt. Home prices have risen for many reasons, including relatively low interest rates and people and businesses treating housing like an investment. But because incomes haven’t kept pace with rising prices, people have had to take on much more debt to buy their homes. In 1990, the average household’s debt was only 90% of its disposable income. By fall 2022, this had more than doubled to 186%.

After the affordability bubble peaked in 1990, house prices in Toronto fell by over 30%. In the rest of Canada, the average home price remained stable throughout the rest of the decade. Stable prices and falling interest rates made home ownership more affordable for a period of time. Economists have been waiting for a similar correction in Canada’s housing market since the financial crisis in 2008, but it never materialized. Whether housing becomes more affordable over the next decade depends on a variety of factors, including interest rates, government housing policy and wage growth.