Canada’s income tax system is progressive: higher-income earners pay a higher percentage of their income in taxes than low-income earners. Local access to income tax revenue could help ease municipalities’ reliance on regressive forms of revenue generation like property taxes and user fees. Canadian municipalities currently don’t have income taxation powers.

A better way

In 2013, the Alberta Urban Municipalities Association formally asked the province to increase income tax rates by one per cent and distribute the money to municipalities based on population.

Highlights

- Is a progressive tax

- Revenues grow with incomes and the economy

- Works best if upper levels of government set rates, collect, and share the taxes

- Difficult to implement locally for medium and small municipalities

Open image in modalHow does it work?

Open image in modalHow does it work?

Municipalities could receive personal or corporate income tax revenue by either getting the power to levy a tax themselves, or by accessing a share of what other levels of government collect.

Direct levying can provide greater control and local accountability over rates and structure, to ensure they are fair and equitable. But direct levying can also create imbalances between closely-situated municipalities, and can be costly to administer on a small scale.

Accessing a share of income taxes levied by senior levels of government may be easiest for administrative purposes. In this case, the province and its municipalities design a specific formula to distribute the revenue based on set criteria, such as population.

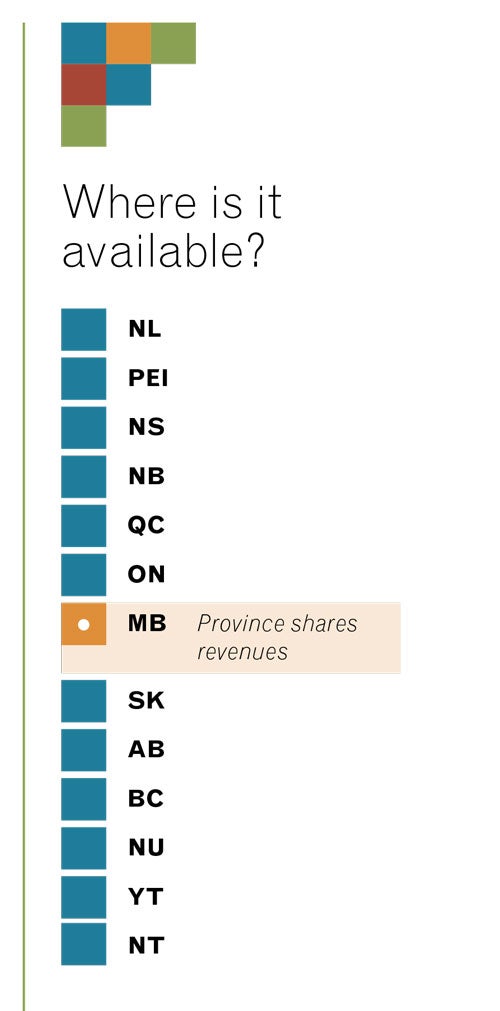

Who uses it now?

While Canadian municipalities don’t have direct income taxation powers, income taxes generate almost as much revenue as property taxes for some municipalities in other countries. For example, New York City raises $9 billion (or 18 per cent of its revenues) from personal income taxes.

Manitoba is the only jurisdiction in Canada that shares a portion of its income tax with local governments, distributing it based on population. Municipalities in Alberta, Nova Scotia, and Newfoundland and Labrador have advocated for access to provincial income tax revenue.

Designating one percentage point of income tax to municipalities in Newfoundland and Labrador could increase local revenues by an estimated 20 per cent. A one per cent tax on incomes in the Greater Toronto and Hamilton area could generate an estimated $1.4 billion annually.