Critics have been fearmongering about unionized workers asking for wage gains that keep pace with inflation, pitting public and private sector workers, as well as unionized and non-unionized workers, against each other. The implication is that raising workers’ wages will make inflation worse. The reality is workers are not responsible for price increases. But, at least in some industries, CEOs are. They have hiked prices unnecessarily, kept employee wage increases low and personally benefited from the resulting profits.

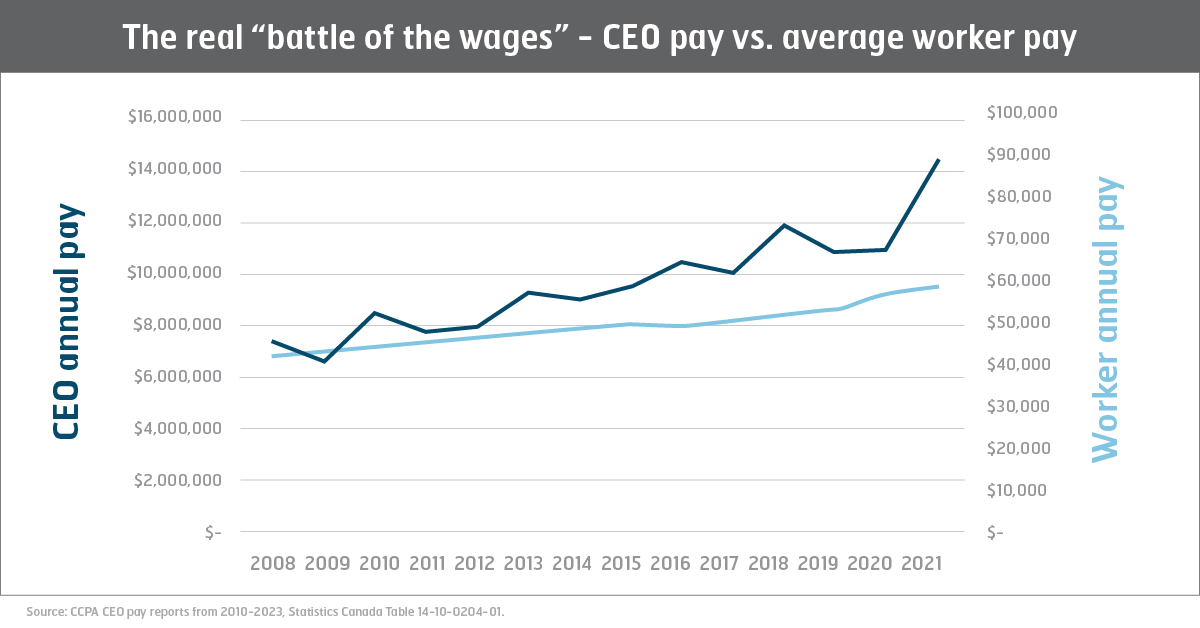

The Canadian Centre for Policy Alternatives (CCPA) has been tracking CEO compensation in Canada since 2008. They compare the earnings of the top 100 CEOs with the average annual salary of workers. In 2008, these CEOs made an average of 174 times more than the average worker, earning $7.3 million annually compared to $42,305. During the pandemic, this ratio reached a new high. In 2021, the top 100 CEOs earned an average of 243 times more than the average worker – $14.1 million a year compared to $58,800. Keep in mind that the average wage for workers increased during the pandemic partly because many low-wage workers lost their jobs. The same was not true for the top 100 CEOs.

The gap is even more significant in specific companies and sectors. For example, Loblaw CEO Galen Weston received $11.8 million in compensation in 2022, which is 430 times more than the average earnings of grocery store workers that year ($27,300).

The CCPA and CUPE have proposed several solutions to address this issue. These include higher tax rates on very high incomes and the full inclusion of capital gains as taxable income (currently only half of capital gains are taxable). Recently, the federal NDP proposed a new strategy modeled on a policy put forward by United States Senator Bernie Sanders. This strategy would increase corporate income taxes for companies based on the difference between CEO and median worker pay. The bigger the gap between CEO and median worker pay, the higher the corporate income tax rate paid.

Some of this policy is already in place in the United States. Following the 2008 financial crisis, the United States implemented the Dodd-Frank Act, which strengthened regulations for banks and publicly traded corporations to enhance economic stability and protect consumers. As part of this legislation, publicly traded corporations are required to disclose the wage gap between their CEOs and other employees. They must identify the median worker, whose income falls exactly in the middle of the employee earnings spectrum. This means that half of employees make more than the median worker, and half less. Companies must then publish the ratio of the median worker’s income to the CEO’s income in their shareholder information before their annual meeting.

In Canada, the financial sector has had discussions about voluntarily adopting a similar practice. The idea is that large disparities in executive and worker pay contribute to growing income inequality. This not only negatively affects the overall economy but also creates governance issues within companies and reduces long-term worker productivity. Desjardins Group, a Quebec-based financial cooperative that encompasses over 200 credit unions, voluntarily discloses the CEO to median worker ratio in its annual report. Vancouver City Savings Credit Union, known as Vancity, publishes two ratios: CEO to median worker and CEO to lowest paid worker. Vancity’s investment arm, Vancity Investment Management, has used its shareholder position to advocate for several Canadian banks and CP Rail to disclose their CEO to median worker pay ratios. So far, only Scotiabank and CP Rail have adopted this practice.

The federal NDP has not yet put forward guidelines for standardizing the calculation of a CEO-worker pay ratio. However, they have proposed a surtax for companies based on this ratio. The surtax would begin at 0.5% if CEOs earn between 50-100 times more than the median worker and increase to 5% if CEOs earn over 500 times more. The NDP estimates that if this were implemented in 2022, Loblaw would have paid an additional $100 million in corporate income taxes.